In a world where economic tides are shifting faster than ever, the real estate market stands as a critical barometer of financial health and opportunity.

A recent conversation between Brent Johnson and Ken McElroy, one of the nation’s foremost real estate investors, offers a rare glimpse into the strategies shaping the future of property investment.

With home prices soaring relative to average incomes and interest rates casting a long shadow, McElroy’s insights reveal a calculated pivot to multifamily properties, a sector he believes is poised for significant growth.

But what’s driving this shift, and how does it fit into the broader economic landscape?

Let’s dive into the dynamics at play and explore why McElroy is betting big on apartments while others hesitate.

The Affordability Crisis: A Tale of Two Markets

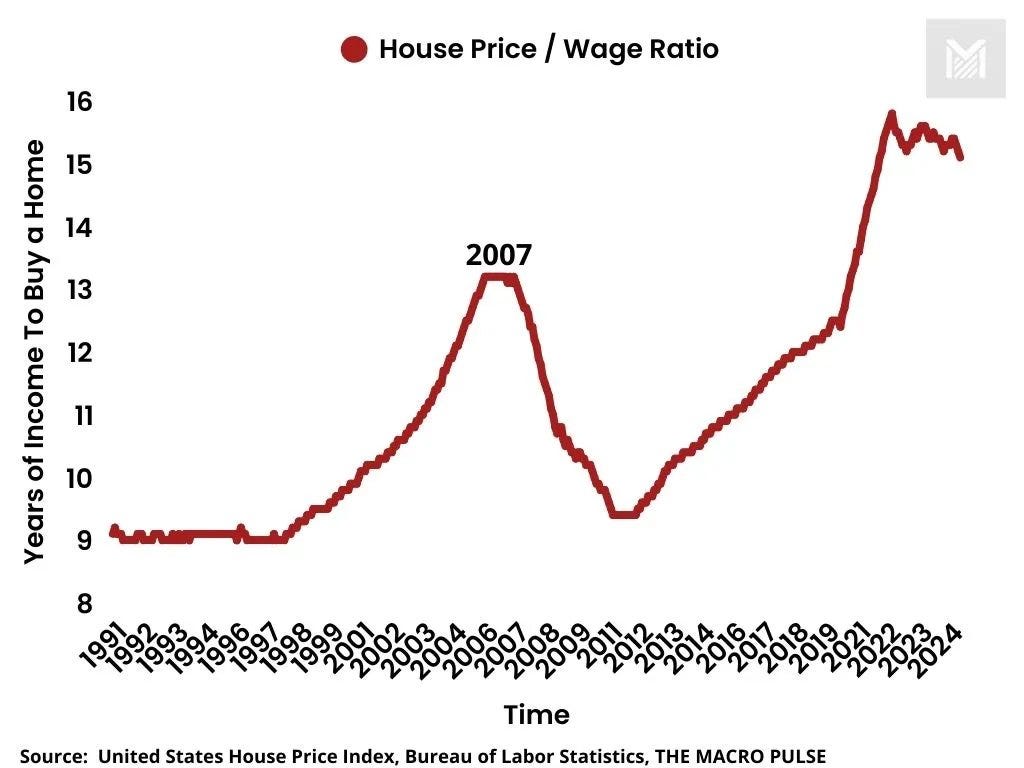

The U.S. housing market is at a crossroads. As was pointed out, the gap between home prices and average incomes has reached historic highs, creating an affordability crisis that’s reshaping consumer behavior.

Single-family homes, once the cornerstone of the American Dream, are increasingly out of reach for many.

With mortgage rates hovering around 6-7% and home prices stubbornly elevated, the math simply doesn’t work for cash flow-focused investors or first-time buyers.

McElroy notes, “The price of homes is high, the price of the mortgage is high, and the rent just doesn’t pay for all of that.”

This mismatch is pushing would-be homeowners and investors alike toward the rental market, particularly multifamily properties.

This shift is more than a trend…it’s a structural change. The average rent for a single-family home might be around $2,000, while a mortgage, plus expenses like taxes and insurance, can easily exceed $4,000.

For investors, this means single-family homes are no longer viable for generating positive cash flow.

Homebuilders, too, face challenges, as evidenced by Lennar’s recent filings, which reveal a reliance on rate buy-downs to make monthly payments palatable for buyers.

These buy-downs, embedded in marketing and sales costs, highlight the lengths to which builders must go to compete in a market where affordability is eroding.

But where does this leave the multifamily sector? McElroy sees it as a golden opportunity.

As single-family homes become less attainable, demand for apartments surges, driven by renters who can’t afford to buy or prefer the flexibility of renting.

This dynamic creates a compelling case for multifamily investments, but the question remains: Is now the right time to buy, or are we on the cusp of a market correction?

McElroy’s Multifamily Play

McElroy’s strategy is clear: he’s doubling down on multifamily properties, with $250 million already invested in existing assets and another $200 million committed to new developments set to open in 2027.

His approach is rooted in a blend of pragmatism and foresight. “I don’t know if it’s quite the bottom,” he admits, acknowledging the possibility of further softening in the market.

Yet, he’s not waiting for the perfect moment. Instead, he’s positioning himself ahead of the curve, likening his nimble operations to a “speed boat” compared to the slow-moving “cruise ship” of institutional investors.

This proactive stance is driven by a key insight: when Wall Street’s big money enters the multifamily space, it tends to push prices higher as competition for quality assets intensifies.

By moving early, McElroy aims to secure properties at below-replacement costs…buildings that would cost more to construct today than their current purchase price.

This strategy not only ensures cash flow at today’s rates but also hedges against future market shifts. “If nothing changes, I’m good,” he says. “If rates go up, I’m still good because I’m fixed. If they go down, I can refinance.”

McElroy’s confidence stems from his ability to lock in favorable financing.

On a recent deal, he secured a fixed-rate loan at 5.18% through Fannie Mae and Freddie Mac, ensuring positive cash flow. This focus on fixed-rate debt mitigates the risk of rising interest rates, a concern that Brent Johnson raised during their discussion.

Johnson, a close observer of interest rates, believes they’re likely to remain elevated or climb higher unless a deflationary crash forces them down, potentially softening real estate prices.

McElroy, however, remains unfazed, betting on the long-term demand for rentals and the inflationary pressures that could drive replacement costs…and property values…higher.

But what happens when the market inevitably shifts? Will McElroy’s bets pay off, or is he walking a tightrope in an increasingly volatile economic environment?

Interest Rates and Tariffs: The Twin Forces Shaping Real Estate

Interest rates are the lifeblood of real estate, influencing everything from affordability to investment returns.

Johnson’s perspective underscores the uncertainty surrounding rates, noting that they could either stay high, rise further, or crash in a deflationary scenario.

Each outcome carries implications for real estate investors.

High or rising rates could strain affordability further, while a deflationary drop might soften prices, creating opportunities for those with cash on hand.

McElroy’s approach sidesteps this uncertainty by focusing on cash flow and fixed-rate financing.

He’s also attuned to another looming factor: tariffs.

With the incoming administration signaling a protectionist stance, tariffs could drive up construction costs, further constraining the supply of new housing.

McElroy anticipates that this will exacerbate the affordability crisis, pushing more people into the rental market and fueling demand for multifamily properties.

“I see the affordability issue still coming,” he says, predicting a “renter nation” where homeownership becomes a luxury for fewer Americans.

This vision aligns with broader market trends.

The National Association of Realtors reported in Q2 2025 that the median home price reached $412,000, while median household income lagged at $81,000, creating a price-to-income ratio not seen since the pre-2008 housing bubble.

Meanwhile, apartment vacancy rates have tightened to 5.8%, according to CBRE, signaling robust demand for rentals.

These numbers underscore McElroy’s thesis: as homeownership slips out of reach, multifamily properties become a safe haven for investors seeking stable returns.

Yet, the specter of institutional investors looms large. When will the “cruise ship” of Wall Street arrive, and how will it reshape the multifamily landscape?

The Institutional Wave: Opportunity or Threat?

McElroy’s strategy hinges on getting ahead of institutional investors, who he expects to flood the market in the coming years.

Historically, large equity groups and hedge funds have entered real estate markets late, driving up prices as they chase yield.

In the multifamily sector, this could create a bubble, pushing acquisition costs beyond the reach of smaller players.

McElroy’s solution is to act now, securing assets before the big money arrives.

His recent moves…four recapitalizations and new developments…reflect a race against time to build a portfolio that can weather the coming wave.

This dynamic raises a critical question: How will smaller investors compete when institutions with deep pockets enter the fray? McElroy’s answer lies in agility and local expertise.

By moving quickly and leveraging his team’s market knowledge, he can identify undervalued properties and structure deals that cash flow immediately.

For example, his focus on buying below replacement cost ensures a margin of safety, while fixed-rate financing protects against rate hikes.

This approach contrasts with homebuilders like Lennar, who are grappling with declining margins as they absorb the cost of rate buy-downs to attract buyers.

But there’s another layer to consider: the competitive tension between rental properties and homeownership.

Homebuilders are pulling out all the stops to lure buyers, offering incentives that individual sellers can’t match.

McElroy sees this as a net positive for the multifamily sector, as it underscores the affordability gap driving renters to apartments.

Yet, he also acknowledges the risk of a market correction.

If single-family home prices fall significantly, it could ease the pressure on rentals, potentially softening demand.

So, how does McElroy plan to navigate this delicate balance?

The Renter Nation: A Long-Term Bet

McElroy’s outlook is grounded in a belief that the U.S. is moving toward a “renter nation,” where homeownership becomes less attainable for a growing segment of the population.

This trend is already evident in demographic shifts: Millennials and Gen Z, burdened by student debt and high housing costs, are renting longer than previous generations.

According to the U.S. Census Bureau, the homeownership rate dropped to 65.3% in 2024, down from 67.4% a decade earlier.

Meanwhile, multifamily construction starts have surged, with over 400,000 units under development in 2025, per Yardi Matrix.

McElroy’s investments are tailored to capitalize on this shift.

By targeting properties with high occupancy rates…90-92%…and securing fixed-rate loans, he ensures steady cash flow while positioning for future rent growth.

He predicts “exponential rent growth” by 2027-2029, driven by persistent supply constraints and rising demand.

However, this forecast comes with a caveat: political backlash.

As rents climb, so too will calls for rent control, a policy that could cap returns for multifamily investors. McElroy is already planning for this, aiming to exit some investments within a three-to-five-year window before such measures take hold.

But what about the wildcard of international capital? Could a weakening dollar or global economic shifts alter the calculus?

A Shift in Capital Flows

One of the most intriguing aspects of McElroy’s conversation with Johnson is the discussion of international buyers.

In past cycles, notably during the 2007-2009 financial crisis, a weak U.S. dollar attracted foreign investors to American real estate, seeking hard assets as a hedge against currency devaluation.

McElroy recalls raising significant capital from Canada when the U.S. and Canadian dollars were near parity.

Today, however, the landscape is different. Global investors are wary of the U.S. dollar, with some opting for gold and Bitcoin over real estate.

“We’re not seeing the international inflow like we were,” McElroy notes, signaling a flight to alternative assets amid geopolitical and economic uncertainty.

This shift complicates McElroy’s strategy but doesn’t derail it.

By focusing on domestic opportunities and leveraging agency debt from Fannie Mae and Freddie Mac, he reduces reliance on foreign capital.

Still, the absence of international buyers could temper price appreciation in some markets, particularly in high-cost coastal cities where foreign investment has historically been strong.

The question is whether domestic demand, fueled by the affordability crisis, will be enough to sustain the multifamily boom.

Volatility and Opportunity

As Johnson and McElroy wrapped up their discussion, they touched on the broader economic outlook for 2025.

Johnson draws parallels to 2022, when rising interest rates triggered market volatility.

He expects similar turbulence in the second half of 2025, driven by tariffs and a “regime change” in how the U.S. engages with global markets.

Tariffs, like interest rate hikes, increase costs, potentially squeezing consumers and businesses alike. For real estate, this could mean higher construction costs and tighter supply, further bolstering the case for multifamily investments.

McElroy, however, remains focused on the fundamentals.

His career, built on navigating cycles of boom and bust, has taught him to prioritize cash flow and adaptability.

By locking in low fixed rates, buying below replacement cost, and anticipating the renter nation trend, he’s positioned to thrive regardless of short-term volatility.

For investors watching from the sidelines, McElroy’s approach offers a masterclass in strategic timing and risk management.

So, what’s the takeaway for the average investor? The real estate market is no longer a one-size-fits-all game. Single-family homes may be trapped in a cycle of high prices and low mobility, but multifamily properties offer a path to steady returns…if you can move fast and think long-term.

As McElroy puts it, “Whatever happens, happens. I’m hedged on the up, and I’ll take advantage on the down.” In a world of uncertainty, that’s a playbook worth studying.

👉 What’s quietly driving the dollar’s next big move...and why could it matter more than rate hikes or headlines? The charts are signaling something… but what?