The Saver's Tax

Why your purchasing power is shrinking even when the rate goes up.

![[Section Divider Image]](https://substackcdn.com/image/fetch/$s_!EZLc!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fbe1f7b9b-3783-457a-980a-0b49d31b960c_1320x50.webp "[Section Divider Image]")

Your savings account is paying interest. Your money market is paying more. Your short Treasury ladder is paying more still. The Fed has not cut its policy rate this year. And every month, your purchasing power keeps going down.

This is the part of the regime that does not get covered. Not because the data is hidden... it is sitting in plain sight in every monthly CPI release, every rent renewal, every grocery receipt. It does not get covered because it is so simple it offends commentary built around the choreography of the next rate decision. The saver’s tax is not a forecast. It is the present tense.

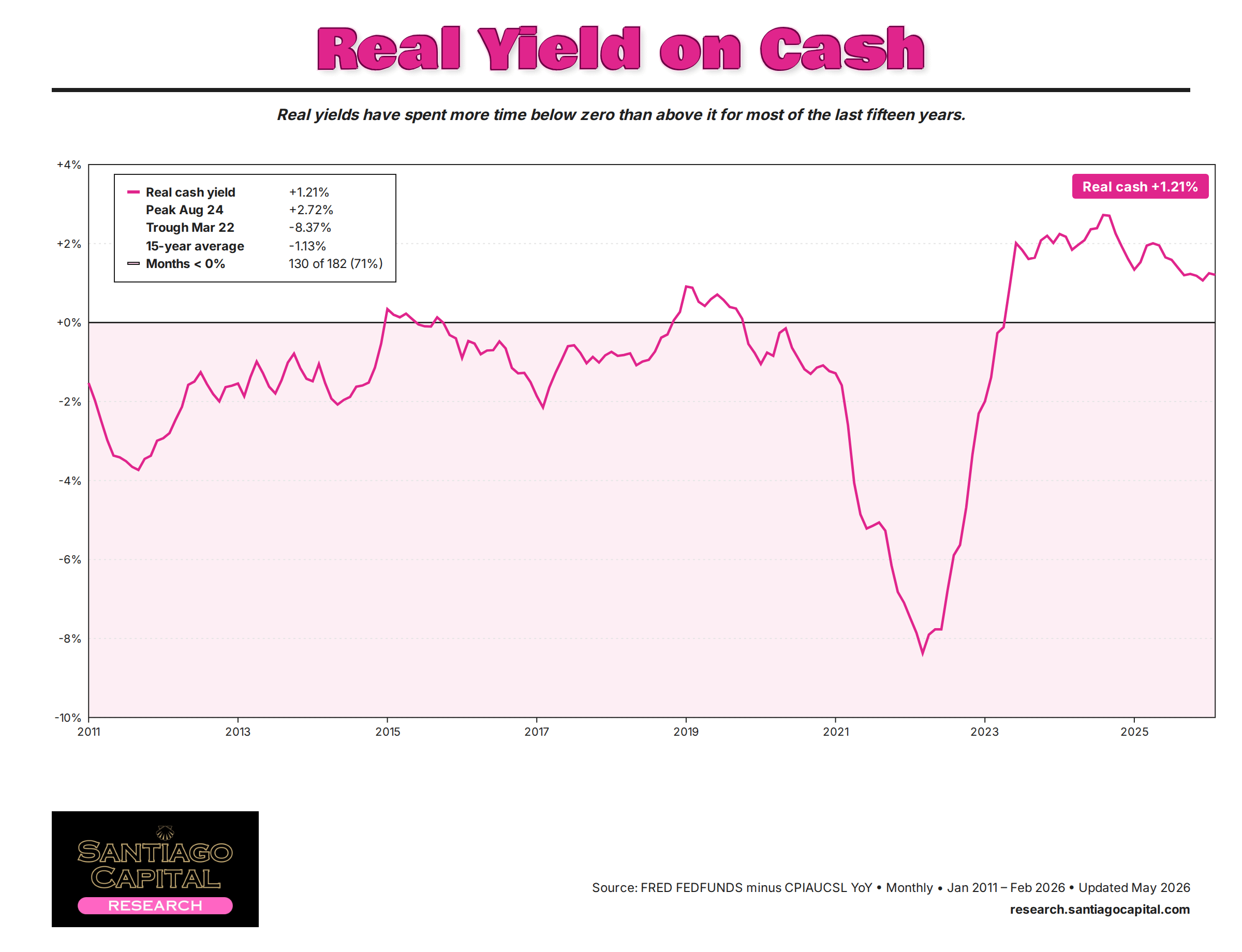

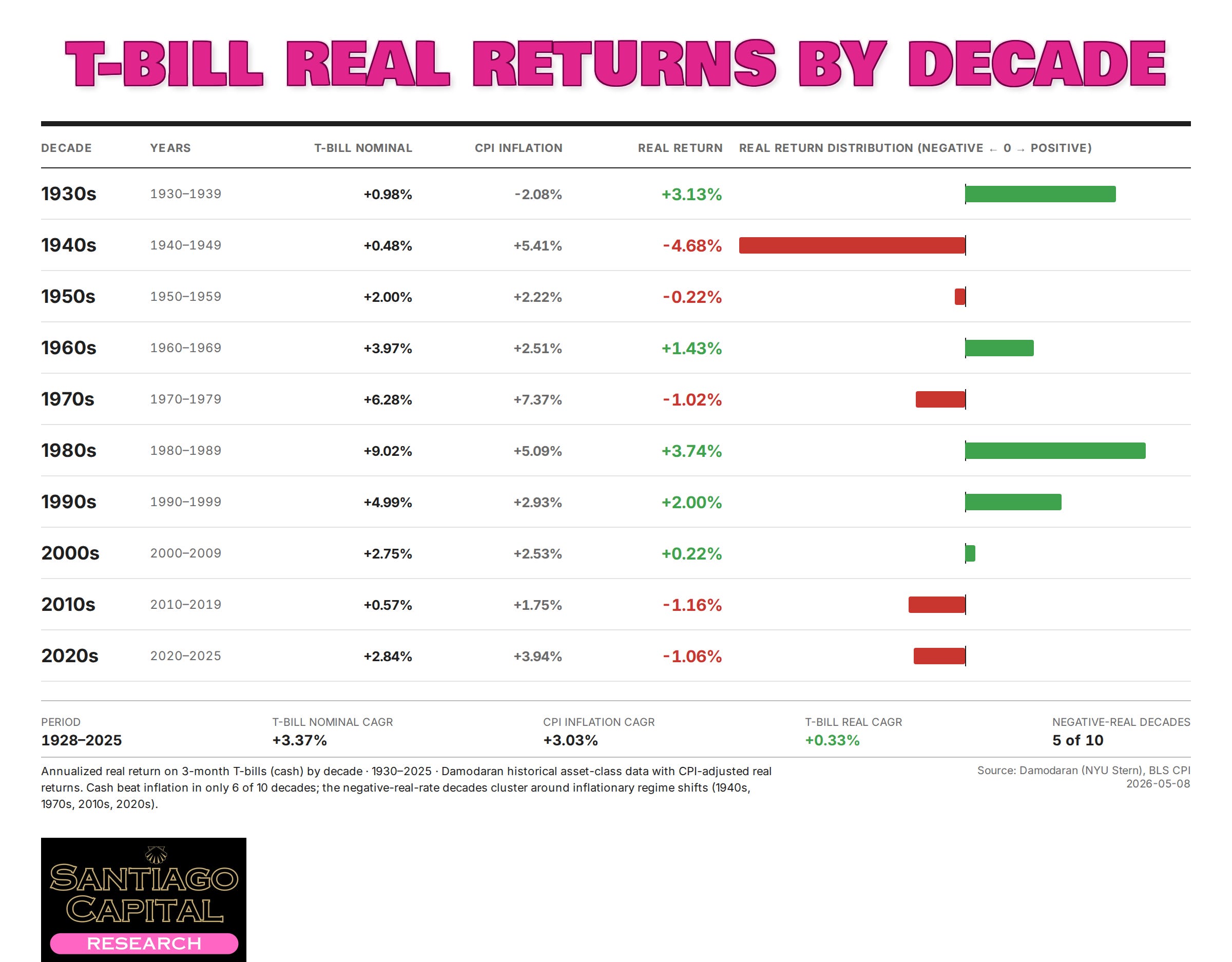

The Real Rate Math On Your Statement

Take the math at its plainest. The real interest rate is the nominal rate minus inflation. Park a dollar in a four-percent instrument. Watch the price level climb five percent over the year that follows. The number on your statement gets bigger. The thing that number can buy gets smaller. You earned a positive nominal return and a negative real one, and the second figure is the one that controls your standard of living.

You see this only as success. The interest accrued. The balance ticked up. The statement comes printed in green. What does not show up on the statement is the price of the gallon of milk, the homeowner’s insurance renewal, the school tuition that just went up nine percent. Your statement is denominated in the unit being debased, which is what makes the tax invisible. The measuring stick moves while you watch the measurement.

None of this is new. None of it is even unusual. Negative real rates are a recurring feature of the historical record, and every prior episode left a documented resolution path. The record is the most useful reading on the table right now.

Why Negative Real Rates Punish Savers Specifically

When real rates are positive, the system rewards patience. When real rates are negative, the system penalizes it. The incentive structure inverts. Three roles take three different sides of the same trade. The saver, holding cash and short-duration instruments, pays. The borrower, sitting on long-duration fixed-rate debt taken out before the regime, collects. The speculator, holding any asset with a supply curve that cannot move with the price, collects. That is mechanics. It is not commentary.

You do not have to believe a single thing about Fed credibility, Treasury issuance, or the trajectory of inflation to see that part. You only have to look at who is paying and who is being paid in the present configuration. The answer is unambiguous, and it has been unambiguous for over a year.

It’s not that holding cash is wrong. There are seasons when the optionality of cash matters more than the carry. There are seasons when the stability matters more than the return. But you have to know the price you are paying for that optionality, and right now the price is being charged through a mechanism most savers never see itemized on a single line of a single statement.

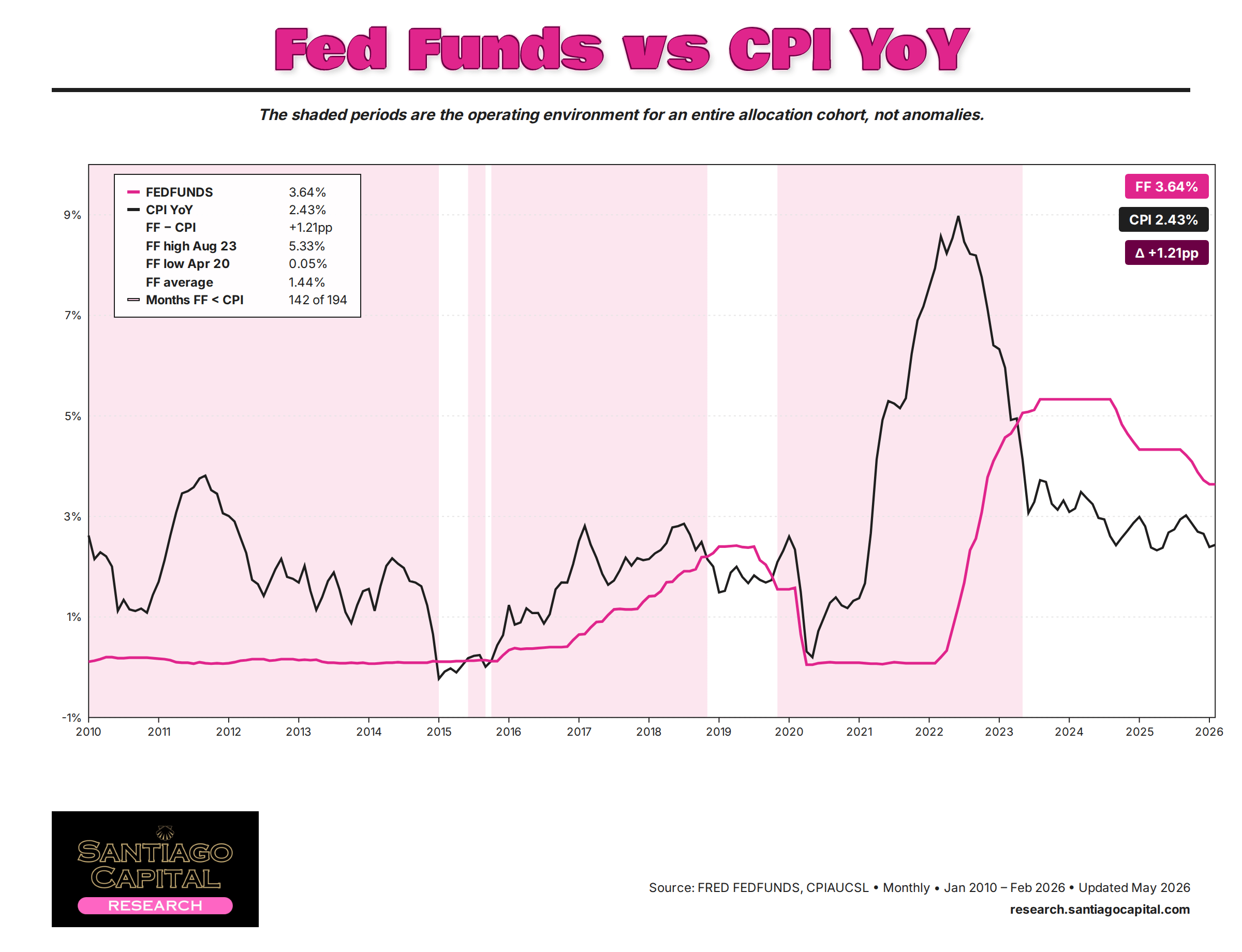

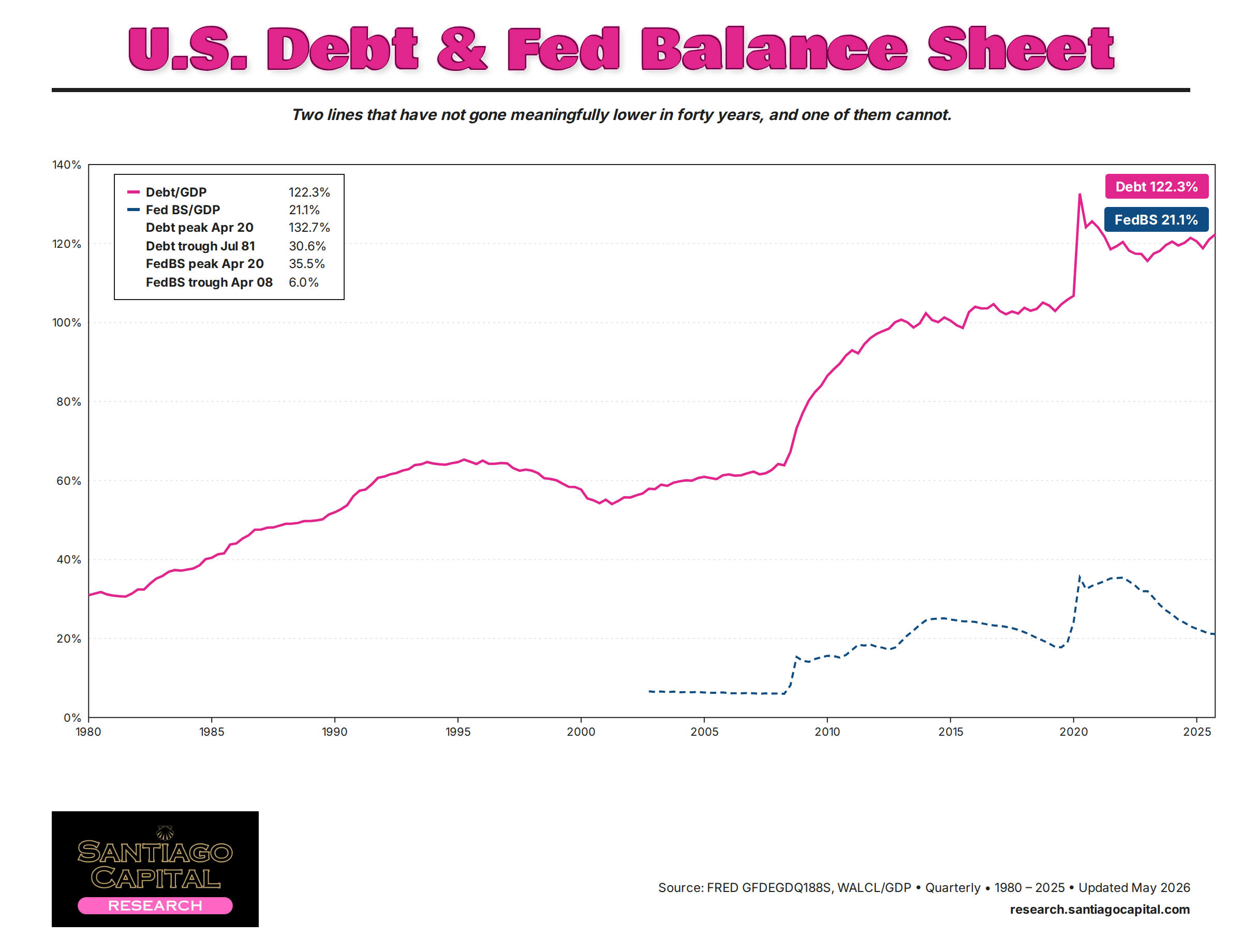

Why Negative Real Rates Are Structural Not Cyclical

This is where the framing matters most. The standard macro narrative treats compressed real rates as a temporary feature of an aggressive easing cycle that will mean-revert once inflation cools. Wait it out. The Fed gets back to two. The real rate normalizes. Cash starts paying again. That is the cyclical reading.

Step away from the cycle commentary on television. Look at what the central banks themselves are signaling in working papers, at what the Bank for International Settlements is publishing on debt sustainability, at how sovereign reserve allocators are repositioning. The framing on the inside is different from the framing on the outside. Compressed real rates are not the consequence of one tightening or easing cycle. They are the consequence of a debt configuration that has been building for forty years and now requires accommodative real-rate conditions to remain serviceable. The accommodation is not optional. It is the cost of carrying the stock of debt the system already owes.

Same people who told you in 2021 that the inflation was transitory are now telling you the negative-real-rate regime is transitory. It is the same construction, one rung higher up the analytical ladder. The transitory is the cycle. The structural is the configuration.

What Negative Real Yields Do to a Standard Allocation

Look at the practical consequence in your own posture. The cash sleeve that used to be a defensive position is now a slow leak. The short Treasury ladder that used to be a conservative yield substitute is now a real-return-negative position dressed up as conservative. The 60/40 portfolio’s foundational assumption, that bonds rally when stocks fall, has been breaking down since 2020. The protection is not what it used to be. We covered that breakdown directly in The End of Peacetime Portfolios, and the case has only sharpened in the year since.

For institutional pools, the pressure shows up in the liability-matching arithmetic. The duration assumption that worked for thirty years rested on real rates mean-reverting to a positive plateau. They have not. The pension funds, insurers, and sovereign wealth allocators sitting on the largest pools of capital in the world have been quietly flagging the problem for two years. Most private investor portfolios have not adjusted.

That is not a coincidence. It is what late-cycle environments look like.

What Less Than Zero Maps That This Article Does Not

You can map the math from this article. You can name the mechanic. You can frame the structural piece. What you cannot do from this article is rank the four prior historical episodes of negative real rates by how each one ended, and then read the present configuration against the four scenarios that fall out of that record. That is the architecture of the report.

What this article does not cover, and what Less Than Zero: The Price of Addiction in a Debt-Based World does:

The four prior episodes ranked by how each one ended, with the cross-asset behavior that defined each resolution

The four scenarios for how the current episode resolves, with the asset-by-asset response in each

The cross-asset framework that has held across every major episode of negative real rates over the past century

A new metaphor that organizes the entire monetary layer underneath the geopolitical and fiscal arguments we have been writing about for over a year

The cost of carrying the right exposures into the resolution scenario that actually plays out is modest. The cost of being positioned for the wrong scenario is not modest, and the asymmetry is not new either.

The framework will tell you when it is time. The framework has been telling you for a while.

→ Read Less Than Zero: https://research.santiagocapital.com/p/less-than-zero

This material is for educational and informational purposes only and is not investment advice. Santiago Capital and Brent Johnson are providing analytical frameworks and commentary on macroeconomic conditions. Nothing in this article constitutes a recommendation to buy, sell, or hold any security or asset. You should consult a licensed financial advisor before making any investment decision.

Enjoying Santiago Capital Research? Share it…and get rewarded.

Our referral program lets paid subscribers earn free service just by spreading the word. Refer 5 readers and unlock a free month of Santiago Capital Research. Refer 15 and earn 3 months free. Refer 30 and get 6 months…on us.

Your referral link is also waiting in the tab below every post. Start sharing today.