Why Gold Just Sold Off

Real rates rose. Gold fell. By the time you read this the price has moved again. The mechanics haven't. The sell-off is the feature, not the bug.

![[Section Divider Image]](https://substackcdn.com/image/fetch/$s_!FVHa!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2Fafcbf425-c4be-43b6-b750-5b2a78a1665d_1320x50.webp "[Section Divider Image]")

![[Section Divider Image]](https://substackcdn.com/image/fetch/$s_!IssG!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F3fe70fdb-2d1e-4f80-9354-636ff3b9e8cb_1320x50.webp "[Section Divider Image]")

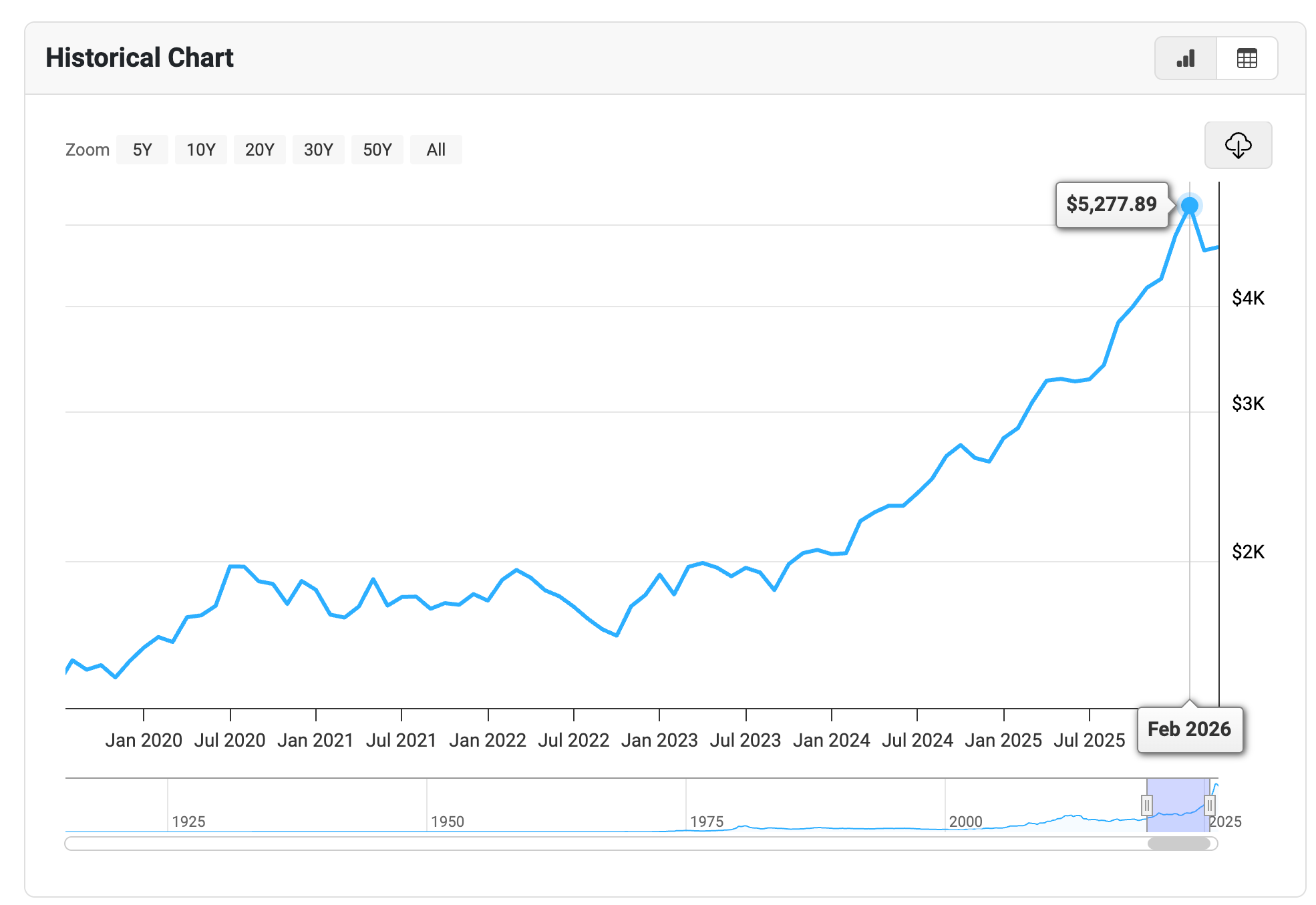

You opened your phone Friday and saw it. Gold closed near $4,724, down 3% on the week.

The pundits will tell you what this means. Inflation expectations rose. The Fed might hike. The dollar firmed. The debasement trade is breaking down.

You don’t have to believe any of that to see what’s actually happening.

By the time you’re reading this, the price has moved again. The mechanics haven’t.

Why Gold Sold Off Last Week

The mechanic is plain. When inflation expectations rise faster than nominal rates, real rates fall and gold rises. When nominal rates rise faster than inflation expectations, real rates rise and gold sells off. Last week was the second case.

The University of Michigan’s five-year inflation expectations ticked up to 3.5%, the highest reading since October 2025. The 10-year Treasury yield closed Friday at 4.31%. With the Warsh hearing pulling the conversation toward a more hawkish Fed posture, traders priced stronger rate-hike risk into the curve. Real yields rose. The opportunity cost of holding a non-yielding asset rose with them. Gold sold off.

That is the textbook explanation. It is also the boring one. The interesting question is what it tells you about the thesis.

The Debasement Trade Was Never Going to Be a Straight Line

Last December’s framework still applies. Fiat currencies are designed to lose value. Hard assets endure. None of that is in dispute.

But the debasement trade isn’t a straight line. Credit contractions happen inside inflationary regimes. Carry trades unwind. Liquidity squeezes hit gold the same way they hit everything else, sometimes harder, because gold is the most liquid hard asset on earth and it gets liquidated first when investors need dollars in a hurry.

If you remember what oil did in 2022, where the consensus said no oil under $90 ever again and oil promptly cut in half, you already know the pattern. A thesis can be structurally correct and still produce violent corrections inside the bull move. Especially when the consensus is loudest.

Gold Was at $5,500 in February

Worth keeping perspective. When silver and gold went parabolic in February, gold traded above $5,500. By Friday the metal had drifted back to roughly $4,724. That was about a 14% drawdown from the February peak.

You aren’t watching the start of a sell-off. You are watching its continuation, ten weeks in. Friday’s 3% print is one bad close inside a longer mean reversion that began after gold went parabolic. The kind of correction that the framework laid out at $4,200 last October flagged as not just possible but expected. Monthly momentum readings at that October peak were more stretched than at any point since 1980. Parabolas unwind. That is what they do.

What the Sell-Off Doesn’t Tell You

Most investors will read the price action as a verdict on the thesis. It isn’t. A 3% week doesn’t resolve the question that matters.

The question that was on the table at $4,200 was this: are you watching a cyclical peak, or are you watching the early innings of a monetary system unraveling? The price tape cannot answer that for you. Only the structural drivers can.

Look at what hasn’t changed. Central banks are still net buyers of gold, and have been accelerating since the 2022 confiscation of Russian reserves rewrote the rulebook on what reserve safety actually means. Less than one percent of American households hold physical gold. The U.S. Treasury still books its reserves at $42.22 per ounce against a market price north of $4,700, a balance-sheet gap of more than 11,000% that nobody discusses openly. The Pentagon’s Office of Strategic Capital is still expanding the critical-minerals list, and gold-and-silver inclusion remains on the table. Sovereign demand for non-dollar reserve assets is structural, not sentimental.

None of that flipped last week. The price did.

It’s Not That the Pullback Doesn’t Matter

It does matter. If you bought at the February high, you are underwater. If your portfolio is more than 25% in gold, the math says you should be trimming. If you are using leverage, you should be careful.

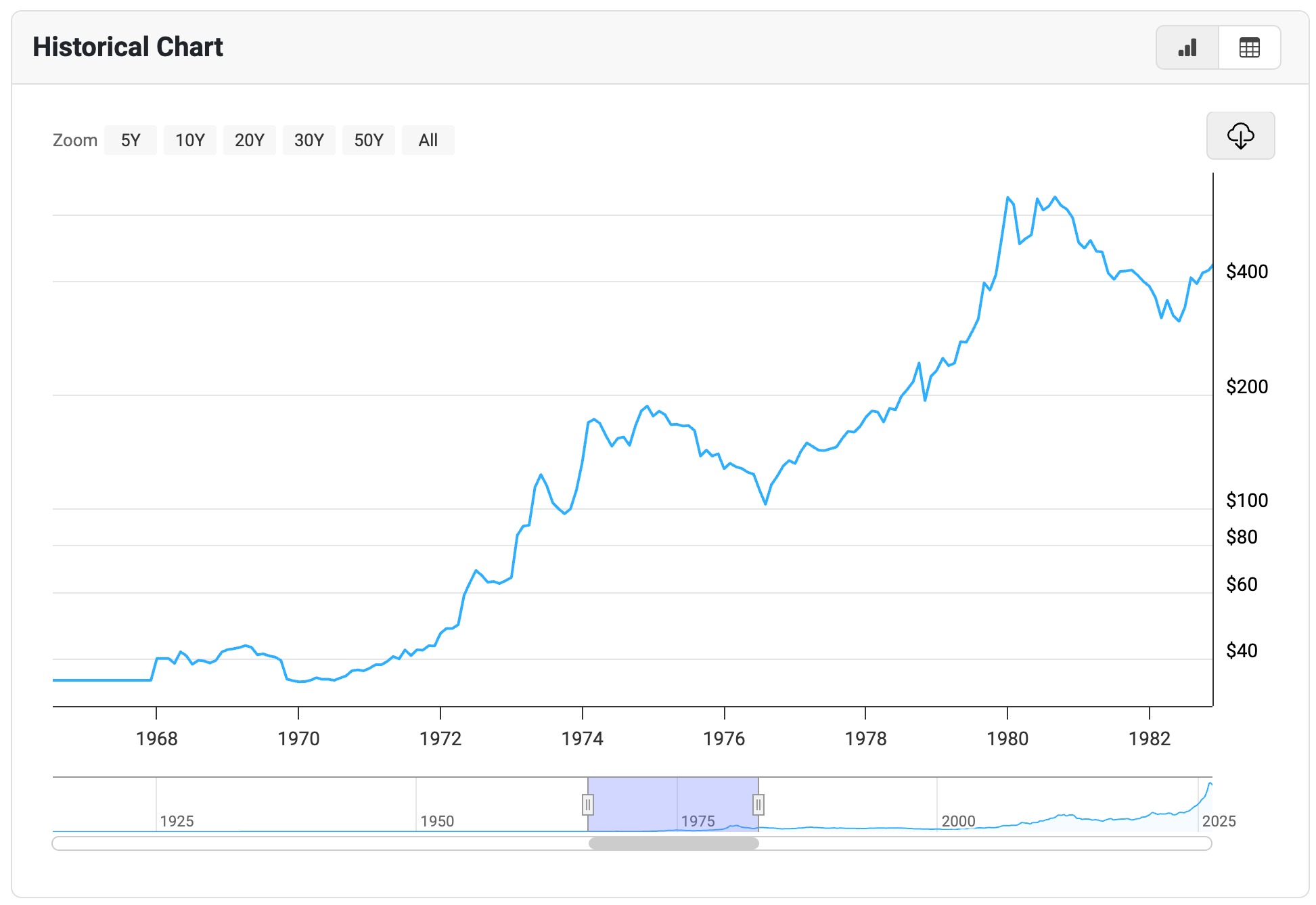

It is just that treating the sell-off as the signal rather than the noise is how investors miss the move that actually matters. Gold sold off 47% in 1976 inside what became a roughly 2,000% nominal gain by 1980. The investors who got shaken out at the bottom of the 1976 correction watched the rest of the move from the sidelines, holding cash that kept losing purchasing power while the metal they sold ran another 700%.

Properties Don’t Change. Prices Do.

Gold’s properties did not change last week. It is still the only element on the periodic table that satisfies every requirement for money. It is still the only asset whose ownership requires no counterparty. It is still what every major central bank on earth is accumulating, what foreign reserve managers are quietly rebalancing into, what sovereigns hoard without commenting.

The price moved. The structural setup did not.

You don’t have to be a bull on the next 3% move to be a bull on the next 30%.

The thesis was never that gold moves up every week. The thesis is that gold answers a question fiat money cannot.

Last week did not change the question.

A 3% sell-off is one data point inside a thesis that has been building since the dollar got weaponized in 2022.

Premium gives you that thesis week by week. The Sunday Macro Pilgrim’s Ledger reads each new print, including gold’s real-rate moves and central bank cross-currents, against the framework you’ve been tracking. The full paid archive carries every prior argument this article extends, including the Debasement Trade piece that explains why corrections happen inside structurally correct theses.

The framework will tell you when it is time.

Gold can rise fundamentally even after sharp pullbacks because the big drivers are structural: central-bank buying, underownership by Western investors, geopolitical stress, and a persistent demand for a neutral reserve asset when trust in fiat weakens.

In my view, the selloff like this is usually more about positioning, leverage, and short-term liquidity than a change in the long-term thesis.

I'm not a paragraph in and I smell AI.